What determines the extent of employers’ wage-setting power? It boils down to how easily — borrowing Beyoncé’s phrase — you can “release your job” when pay isn’t good enough. But how simple is it for someone to quit Walmart if they are dissatisfied with their wage?

To answer this question, my collaborators Suresh Naidu and Adam Reich and I surveyed about 10,000 Walmart workers in 2019 using a Facebook-based strategy, similar to the Shift Project. As we saw previously, Walmart, the nation’s largest private employer, has long been associated with low pay. In 2019, its voluntary company-wide minimum wage stood at $11 per hour, lagging behind competitors like Target and Costco. If paying jobs were truly easy to replace, one would expect Walmart jobs to be among the easier to quit and move on from, or market pressure would already have pushed Walmart wages to match those competitors.

To make an apples-to-apples comparison, here I focus on roughly 1,300 workers earning exactly $11 in states where that wage was legal (i.e., the state minimum wage was below $11). We asked these workers how easy it would be to find a new job at least as good as their current one. The results were striking. Only 36% said it would be “very easy” or “somewhat easy” to get a comparable job — meaning nearly two-thirds felt it wouldn’t be easy at all. Even in higher-wage Northeastern states, where $11 was relatively low, 42% still said that replacing their $11/hour Walmart job wouldn’t be simple. The common belief that low-paying jobs are easy to leave and replace just doesn’t match the reality many workers face — even at Walmart.

The quit elasticity

We can get a better sense of how hard it is for workers to quit by looking at how pay affects the chances of leaving a job. To see this in action, let’s look at Marta and Petra, [two fictional workers drawn from real administrative data provided by the Oregon Employment Department]. Marta ended up at Walmart, earning 75 cents less per hour than Petra, who got a job at Target. If we track how long they each stick with their jobs, it can tell us a lot about how competitive the job market really is. In a truly competitive labor market, Marta would quickly jump ship for a better opportunity. But if she sticks around almost as long as Petra, that suggests the market is more “monopsonistic” — Walmart can pay less without losing all of its workforce.

[Editor’s note: In the labor market, a “monopsony” refers to a situation where a single employer, such as Walmart, has outsized power to set wages, driving pay below competitive levels. The term was coined by the British economist Joan Robinson to mirror monopoly, but on the buyer’s side of the market.]

Why would this matter? In a hypercompetitive world, a 5% lower wage than competitors should send workers running for the exits, pushing employers to raise pay closer to workers’ productivity. But real-world evidence suggests this is rarely the case.

Based on our data, Marta’s 5% lower wage at Walmart would nudge her monthly quit rate up a bit to 7%, compared to Petra’s 6.5% at Target. That’s a difference, but nowhere near the mass departures predicted by the textbook competitive model. On average, Marta might stay at Walmart for about 14 months, compared to Petra’s 15 months at Target — a modest gap. For labor economists, this simple comparison says a lot about what’s really going on in the job market. Companies that pay less do face higher turnover, but not massively so.

It might seem bland at first glance, but this sensitivity of quits to wage changes is a spicy measure of labor market power. Economists often use elasticities to put a single number on how responsive one thing (like quits) is to changes in another (like wages). The quit elasticity answers, “If a firm changes wages by 1%, by what percent do quits go up or down?” In other words:

Quit Elasticity = % Change in quits / % Change in wages

A large (negative) elasticity, say -10, would mean most workers bolt at the slightest pay cut — classic high competition. A smaller magnitude, like -1, indicates a fair amount of monopsony power: Workers aren’t as quick to quit, so companies can keep wages lower without losing everyone.

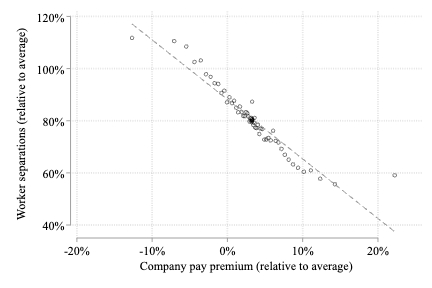

Let’s apply this to our data. A 5% lower wage boosted the monthly quit rate from 6.5% to 7.0%, a jump of roughly 7%. Dividing 7 by 5 gives a quit elasticity of -1.4. That’s miles away from the hypercompetitive model and indicates that retailers like Walmart or Target have notable wage-setting power. This is what we found in our data on low-wage industries like retail and food services. When we expanded our analysis to include workers across the economy, we found a general quit elasticity of around -2. [The graph below] illustrates the underlying calculations: If a company pays 10% less than a competitor, quits will be about 20% higher. Employers can opt for a lower-pay position without hemorrhaging workers.

In case you are wondering, monopsony is not just a rural or small-town story. We found the labor market in the Portland metro area to be a little bit more competitive than the rest of the state, but it was still well below anything close to the competitive ideal — proving monopsony power exists even in big cities with more employers to choose from.

So far, we’ve focused on quits. But wage changes also affect how easily a firm can recruit new workers. The elasticity of labor supply to a firm combines the recruitment and separation elasticities (by adding up their magnitudes), showing how much the overall workforce expands or shrinks if a firm offers higher or lower wages.

Now, for various data-related reasons, estimating recruitment elasticities is more challenging, though recent studies have begun to make headway. Still, economist Alan Manning (arguably the dean of monopsony scholars) has very helpfully shown that under certain assumptions, the recruitment elasticity tends to be similar in magnitude but opposite in sign to the quit elasticity. The reasoning is straightforward: Many new hires at one firm are workers quitting another. As a result, when you add the quit and recruit elasticities together, the total labor supply elasticity ends up being roughly twice the quit elasticity, but with the opposite sign. So in our Oregon case, a quit elasticity of -2 implies a labor supply elasticity of about 4 — far below what you’d expect in a highly competitive, frictionless labor market.

Ultimately, seeing how little wage differences affect quits tells us that labor markets aren’t as fluid as many free-market adherents might predict.

Once you do the math, this range of labor supply elasticity suggests that firms get away with paying only about 80% of what workers would earn in a truly competitive market. The other 20% goes to companies as higher profits or covers turnover and recruitment costs. Monopsony explains why less productive companies can survive in the market, paying lower wages than better-paying competitors. Yes, they will have higher turnover, but not inordinately so.

Monopsony also helps explain why wages can vary across employers with similar productivity. Some adopt a low-wage, high-turnover approach, while others aim for higher wages and lower turnover. Both can be profitable, but one is clearly more worker-friendly.

Ultimately, seeing how little wage differences affect quits tells us that labor markets aren’t as fluid as many free-market adherents might predict. That’s why the quit elasticity — and the broader notion of monopsony power — is vital for explaining how wages are set in the real world and why some jobs simply pay better than others, even when the workers are equally qualified.

Provost Professor of Economics at the University of Massachusetts Amherst

The Energy Transition